Choosing a merchant services company is one of the most important financial decisions a business owner can make. The right provider can help you accept payments smoothly, control processing costs, access reliable point-of-sale technology, and improve daily operations.

The wrong provider can leave you dealing with hidden fees, long-term contracts, outdated equipment, poor customer support, and unexpected cancellation charges.

Merchant services agreements are often filled with technical terminology, complicated pricing tables, and conditions that may not be clearly explained during the sales process. Before signing an application or agreement, business owners should understand exactly what they are receiving, what they will pay, and what happens if they decide to leave.

Below are the most important questions to ask before signing up with a merchant services company.

1. What Pricing Model Will I Be Using?

Do not simply ask, “What is my rate?” Merchant processing costs usually involve more than one percentage.

Ask the provider which pricing model will apply to your account. Common options include:

- Flat-rate pricing

- Interchange-plus pricing

- Tiered pricing

- Cash discount pricing

- Credit card surcharging

- Subscription-based processing

With flat-rate pricing, the business pays a fixed percentage and transaction fee. This model can be easy to understand, but it may not always be the least expensive option.

Interchange-plus pricing separates the card network’s interchange cost from the processor’s markup. It can offer greater transparency, particularly for businesses with higher monthly processing volume.

Cash discount and surcharging programs are designed to reduce or offset the merchant’s card-processing expenses. However, these programs must be implemented correctly, with appropriate signage, receipt disclosures, pricing practices, and card-brand compliance.

Ask the provider to explain the pricing model using real examples based on your average transaction amount and monthly sales volume.

2. What Is the Total Effective Processing Rate?

A low advertised rate does not always represent the amount you will actually pay.

For example, a provider may advertise a rate starting at 1.5%, but only certain regulated debit transactions may qualify for that rate. Rewards cards, business cards, premium cards, online payments, keyed transactions, and American Express transactions may cost more.

The effective rate is calculated by dividing the total processing fees by the total card-processing volume.

If you processed $20,000 and paid $600 in total processing fees, your effective rate would be 3%.

Ask the merchant services company to provide an estimated effective rate that includes:

- Percentage-based processing costs

- Per-transaction charges

- Monthly account fees

- Statement fees

- PCI-related fees

- Software fees

- Gateway fees

- Equipment charges

- Batch fees

- Other recurring costs

This will give you a more realistic picture than focusing on one advertised percentage.

3. Are There Any Monthly or Annual Fees?

Some processing companies advertise attractive rates but add several monthly or annual charges.

Ask for a written list of every possible fee associated with the account. These may include:

- Monthly service fees

- Monthly minimum fees

- Annual fees

- Statement fees

- PCI compliance fees

- PCI noncompliance fees

- Regulatory fees

- Batch settlement fees

- Online gateway fees

- Virtual terminal fees

- Equipment insurance fees

- Software subscription fees

- Chargeback fees

- Account update fees

Not every fee is necessarily unreasonable. The important issue is whether the provider explains the charges clearly before you sign.

Request a sample monthly statement or pricing schedule so you can see how the charges may appear.

4. Is There a Long-Term Contract?

Some merchant services agreements automatically lock businesses into terms of three years or longer.

Ask these questions:

- Is the agreement month-to-month?

- What is the initial contract length?

- Does the agreement automatically renew?

- How much notice is required to cancel?

- Can I cancel at any time?

- Is there an early termination fee?

A flexible month-to-month agreement is generally easier for a business owner to manage because it allows the relationship to continue based on service quality rather than contractual pressure.

Read the agreement carefully. A sales representative may say there is “no contract,” while the paperwork may still include a fixed term, automatic renewal clause, equipment lease, or cancellation notice requirement.

The written agreement controls the relationship, not verbal promises.

5. Are There Any Cancellation Fees?

Early termination fees can range from a fixed amount to a much larger calculation based on the processor’s expected future revenue.

Some agreements contain a liquidated damages clause. This may require the merchant to pay estimated processing fees for the remaining contract term.

Ask the provider to identify the exact cancellation language in the agreement.

Ideally, the agreement should clearly state:

- No early termination fee

- No cancellation charge

- No liquidated damages

- No hidden deconversion fee

- A reasonable account-closing procedure

Also ask whether equipment must be returned and whether there are charges for missing, damaged, or unreturned devices.

6. Is the Equipment Free, Leased, Rented, or Provided Under a Placement Program?

The word “free” can mean different things in the merchant services industry.

A provider may offer equipment through:

- An outright purchase

- A monthly rental

- A non-cancellable equipment lease

- A free equipment placement program

- A processing-volume commitment

- A promotional reimbursement

Ask who legally owns the equipment and what happens if you close your account.

Under a free equipment placement program, the processor or merchant services provider may retain ownership of the device. The business can use it without purchasing it but may need to return it when processing services end.

Make sure you understand:

- Whether there is an upfront equipment cost

- Whether there is a monthly rental

- Whether the device must be returned

- Who pays return-shipping costs

- Whether damaged equipment creates a charge

- Whether equipment replacement is included

- Whether software fees are separate

Avoid signing a lengthy equipment lease unless you fully understand the total cost. A terminal that appears affordable at a low monthly payment may cost significantly more over a multi-year lease.

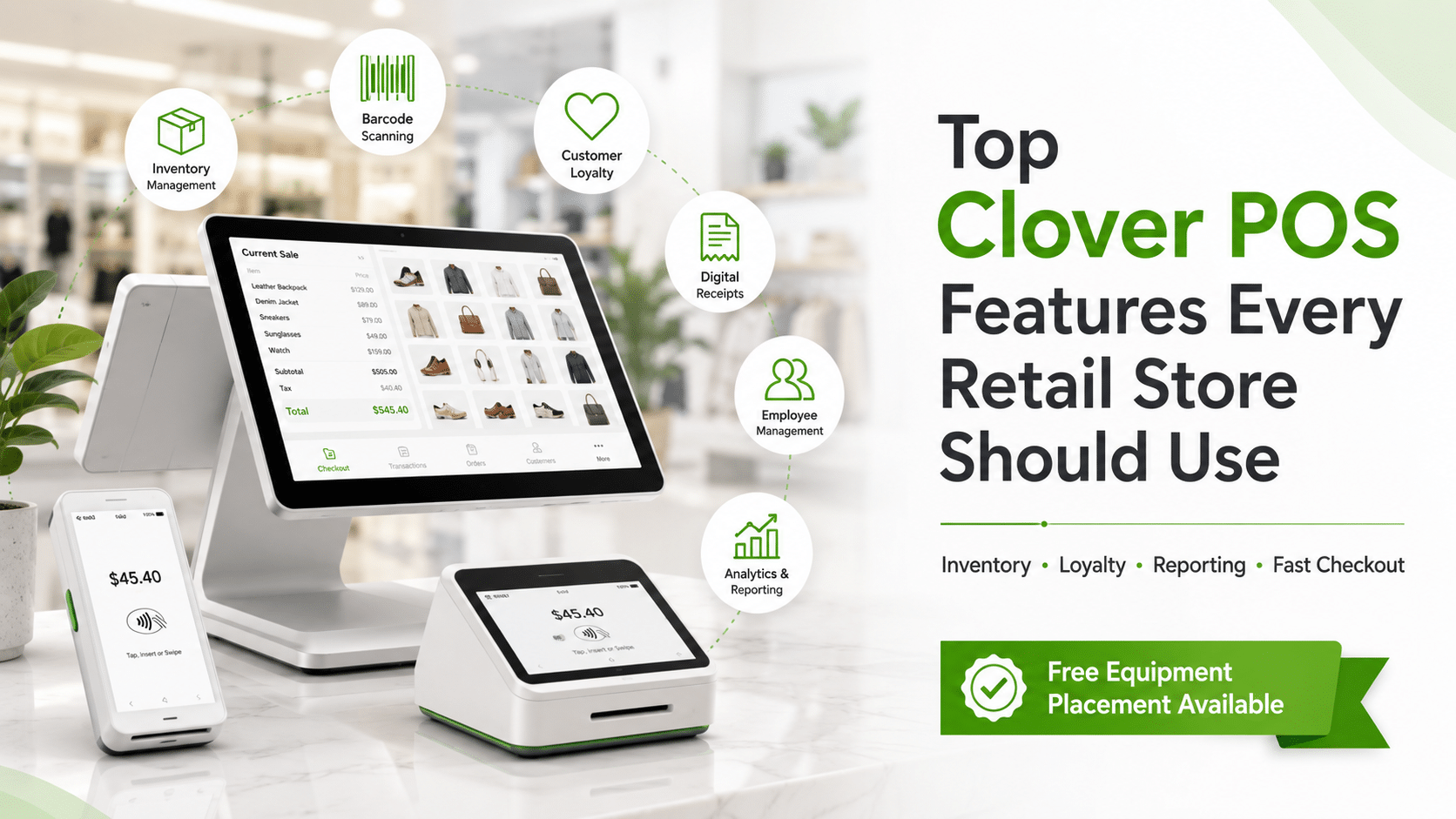

7. Which Point-of-Sale System Will I Receive?

Not every POS system is appropriate for every business.

A restaurant may need tableside ordering, kitchen printing, modifiers, menu management, tipping, and employee permissions. A retail store may need inventory tracking, barcode scanning, purchase orders, and customer management. A salon may need appointments, service menus, staff scheduling, and online booking.

Ask the provider for the exact manufacturer and model of the equipment.

For example, if you are being offered a Clover system, confirm whether you are receiving a Clover Station Duo, Clover Mini, Clover Flex, or another model.

Ask whether the system supports:

- Inventory management

- Employee access controls

- Digital and printed receipts

- Refunds and voids

- Discounts and taxes

- Customer profiles

- Online ordering

- Appointment booking

- Kitchen printers or displays

- Barcode scanners

- Cash drawers

- Accounting integrations

- Sales reports

- Remote access

Do not accept vague descriptions such as “a free terminal” or “a complete POS system.” Get the exact equipment details in writing.

8. Are Software Fees Included?

POS hardware and POS software are usually priced separately.

A provider may offer free equipment while the merchant still pays a monthly software subscription. This is common and not necessarily a problem, but the cost should be disclosed clearly.

Ask:

- What software plan is included?

- How much does it cost each month?

- Can the software price increase?

- Which features are included?

- Are additional apps required?

- Are there separate fees for payroll, online ordering, loyalty programs, or appointments?

- Can I downgrade the software plan?

Compare the software features with your actual business needs. Paying for advanced features that you never use can unnecessarily increase your monthly expenses.

9. How Quickly Will I Receive My Funds?

Funding speed can affect cash flow, especially for restaurants, retailers, contractors, and businesses that need to purchase inventory regularly.

Ask when deposits will reach your bank account.

Important questions include:

- Is next-business-day funding available?

- Is same-day funding available?

- Are weekend deposits supported?

- What time must I close the batch?

- Are there fees for faster funding?

- Can funding be delayed because of holidays?

- What could cause a processing hold or reserve?

A provider should also explain whether unusual transactions, sudden volume increases, large tickets, or a change in business activity could delay funding.

10. What Happens With Chargebacks?

A chargeback occurs when a cardholder disputes a transaction through the card issuer.

Ask the merchant services company:

- How will I be notified about chargebacks?

- How much time will I have to respond?

- Is there a chargeback fee?

- Will the disputed amount be withdrawn immediately?

- Can I upload evidence online?

- Will your team help me respond?

- What steps can I take to reduce disputes?

A good provider should help merchants understand proper receipts, refund policies, transaction descriptions, address verification, signature requirements, and other fraud-prevention practices.

However, no processor can guarantee that chargebacks will never occur.

11. What PCI Compliance Support Is Provided?

Payment Card Industry Data Security Standard compliance, commonly called PCI compliance, helps businesses protect cardholder information.

Ask whether the provider offers:

- A PCI compliance questionnaire

- Vulnerability scanning when applicable

- Compliance reminders

- Assistance completing the required steps

- Data-security guidance

- Breach-response information

Also ask about any PCI compliance or noncompliance fees.

Even when a processor provides tools, the merchant is still responsible for following secure payment practices. Businesses should avoid writing down complete card details, sharing login credentials, using weak passwords, or processing payments through unauthorized devices.

12. Does the Provider Support All the Payment Types I Need?

Confirm that the system supports the payment methods used by your customers.

Depending on your business, these may include:

- Visa

- Mastercard

- Discover

- American Express

- PIN debit

- Contactless cards

- Apple Pay

- Google Pay

- EBT

- Gift cards

- Online payments

- Recurring billing

- Invoices

- Payment links

- Virtual terminal transactions

Also confirm whether the pricing is different for card-present, keyed, online, recurring, or manually entered transactions.

13. Who Provides Customer Support?

Reliable support is essential when your payment system is not working.

Ask:

- Is support available 24/7?

- Is support based in the United States?

- Can I speak with a live representative?

- Who handles hardware problems?

- Who handles funding questions?

- Who handles chargebacks?

- Is training included?

- Will someone help set up my menu or inventory?

- What happens if my device stops working?

Some merchant services relationships involve several companies, including the sales organization, payment processor, acquiring bank, gateway provider, and POS manufacturer.

Make sure you know whom to contact for each type of issue.

14. Can You Provide Everything in Writing?

Never rely entirely on verbal promises.

Request written confirmation of:

- Processing rates

- Transaction fees

- Monthly fees

- Equipment provided

- Software costs

- Contract length

- Cancellation terms

- Funding schedule

- Setup or installation services

- Special promotions

- Free products or services

If a promise is important to your decision, it should appear in the agreement, quotation, email, or official pricing document.

15. Can I Review the Agreement Before Signing?

A reputable merchant services company should allow you to review the agreement before signing it.

Do not allow a salesperson to rush you through the application. Take time to examine:

- The fee schedule

- Contract duration

- Auto-renewal language

- Cancellation procedures

- Equipment terms

- Personal guarantee language

- Reserve rights

- Funding-hold provisions

- Chargeback obligations

- Data-security requirements

Ask questions about any term you do not understand. For larger or more complicated agreements, consider requesting guidance from a qualified attorney or financial professional.

Red Flags to Watch For

Be cautious when a merchant services representative:

- Refuses to provide pricing in writing

- Focuses only on one low rate

- Avoids discussing the contract term

- Pressures you to sign immediately

- Promises that every transaction will qualify for the same rate

- Says equipment is free but cannot explain the ownership terms

- Hides software or monthly account fees

- Claims chargebacks are impossible

- Cannot explain who processes the payments

- Leaves blank spaces in the agreement

- Asks you to sign documents you have not reviewed

Transparency before the sale is often a strong indicator of the service you may receive after the account is opened.

Final Thoughts

The best merchant services company is not necessarily the one advertising the lowest percentage. It is the provider that offers transparent pricing, suitable equipment, clear contract terms, dependable support, and a payment solution that matches your business.

Before signing, compare the total cost rather than one advertised rate. Ask about equipment ownership, software fees, funding times, cancellation conditions, chargebacks, PCI compliance, and customer support.

At Merchant Marvels, we believe business owners should understand their payment-processing program before enrolling. Our free equipment placement options are designed to help qualifying businesses access modern POS technology without purchasing expensive equipment upfront. Available programs may include Clover POS solutions, transparent pricing options, setup assistance, training, and flexible service terms.

The exact equipment, processing program, software plan, and pricing depend on the business type, processing history, approval, and operational requirements.

Before choosing any provider, ask questions, review the written terms, and make sure the solution supports both your current operations and your future growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}